For the first 30 or so years of working, saving and investing, you’ll be first in the mode of getting out of the hole (paying down debt), and then building your net worth (that’s wealth accumulation.). But don’t forget, wealth accumulation isn’t the ultimate goal. Decumulation is! (a separate category here at the Hub).

Corporate tax cuts were a focal point of Donald Trump’s campaign — and Trump says lowering corporate taxes will be a priority in his first 100 days as president.

Based on the initial market response to Trump’s victory, lowering tax rates looks to us like the most important factor driving the market.

Equity markets, of course, like it when taxes are cut. It naturally means more after-tax earnings that can be reinvested or distributed to shareholders — and, importantly, an improvement in valuation ratios that many think look extended under present circumstances.

Lower Tax Rates = Big Earnings Growth and Market Moves in Small Caps

To summarize the results, a simple model shows the following: the more earnings (and taxes paid) that come from the U.S., the greater the earnings growth would be from a tax cut, because by and large, the companies with revenue across the world already have lower effective tax rates. Continue Reading…

Financial author David Bach introduced the Latte Factor as a metaphor for all the small indulgences we regularly treat ourselves to that add up over time. It wasn’t meant to single out Starbucks as the main culprit for our financial woes, but somehow millennials feel the need to stand up for their beloved coffeehouse and defend their right to buy an obnoxious drink whenever they damn well please.

Helaine Olen (not a millennial) made people feel good about buying lattes again when, in her best selling book, Pound Foolish, she explained how the Latte Factor is a lie and buying coffee every day is not why you’re in debt. No, instead it’s the big things: housing, transportation, health care (in the U.S.) that are more difficult to cut back on.

More recently, this author whined about how millennials were being judged on their spending choices, criticizing a survey that revealed millennials spend more on coffee than on saving for retirement:

“Millennials are continually being accused of wasting money on supposedly frivolous things. In October, an Australian man named Bernard Salt wrote that he had had enough of seeing young people ordering “smashed avocado with crumbled feta on five-grain toasted bread at $22 a pop and more. Twenty-two dollars several times a week could go towards a deposit on a house,” wrote Salt.

According to my calculation, if millennials were to abstain from their avocado toast three times a week, they’d save around $3,432 per year. Which isn’t all that much, in reality.”

Oh really? And in what reality is $3,432 not that much money? According to the author, life is unfair and millennials should just give up on the idea of owning a home, or saving for retirement, so just let them have their damn latte and $22 toast.

“Life,” philosopher Albert Camus contended, “is the sum of all your choices.”

Do you think otherwise?

Good or bad. Easy or hard. Right or wrong. Every choice you make will impact your life to some degree.

Choices with little impact are often made without much thought and the trouble is this casual approach to decision making tends to be deployed on bigger and more impactful choices.

In my profession, as a retirement income specialist, I see poorly made choices all the time. They, unfortunately, tend to be life altering, irreversible and totally avoidable. Like a doctor passing along a gloomy prognosis, I am heartbroken to see the look on peoples’ faces when I tell them how a choice they made will put them at a disadvantage for the rest of their lives.

And, as I said, many of these damaging financial choices are often avoidable.

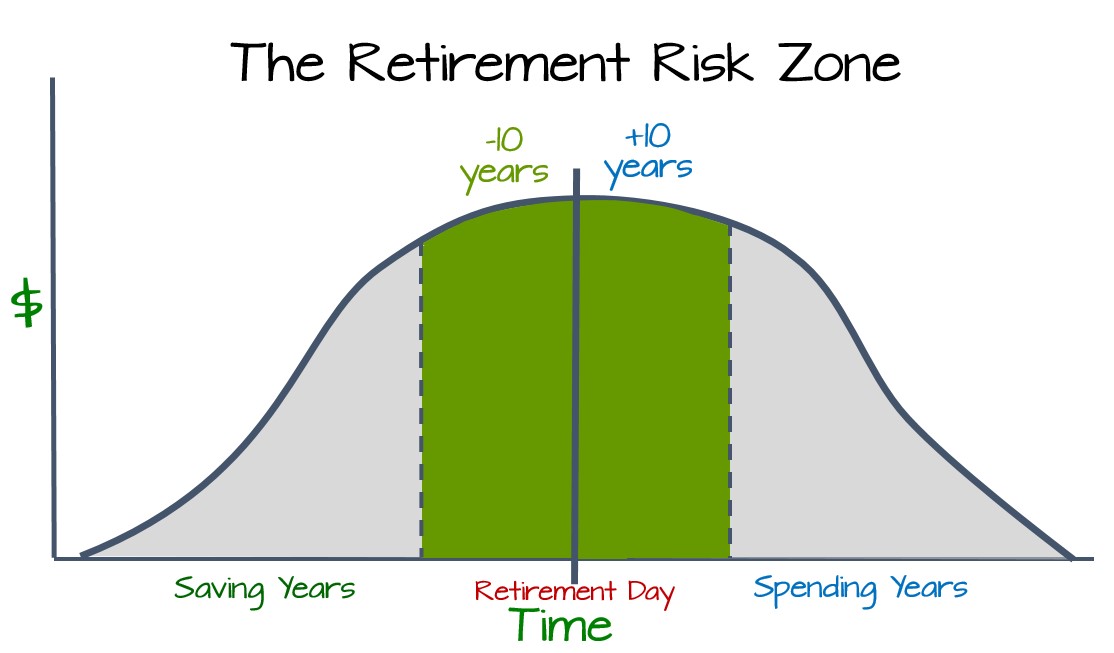

The Retirement Risk Zone Years (TRRZY)

The years leading up to, and the early years of retirement are packed with important choices that can create turning points in your life. We call this period of your life ‘The Retirement Risk Zone Years’ (TRRZY).

TRRZY has aptly earned this acronym because this phase of life contains the highest concentration of high-impact choices that can lead to turning events, both good and bad, in people’s lives.

It is important to recognize that the number and frequency of tough and important choices increases during this time. In addition, the implications of choosing poorly intensify as both time and flexibility have turned from friend to foe. Successfully creating your best possible retirement years is directly linked to how well you navigate the challenging choices of TRRZY.

Over this nearly two-decade period we must adapt our thinking to a new reality. Strategies that served us well during our savings years can turn on their heads and start to work to our disadvantage as our flow of funds reverses from saving to spending. Those who fail to recognize and adapt to this new thinking have a high propensity for making poor choices, many of which they will regret in future years.

Over at MoneySense, my latest Retired Money column has been published, and it looks at the closely related topic of LIRAs (Locked-in Retirement Accounts, which have been termed “the RRSP’s less flexible cousin.” You can find the full column by clicking on this highlighted headline: Unlocking the Mystery of LIRAs.

In a nutshell, LIRAs are also known in some provinces as Locked-in RRSPs, which is exactly what they are. Unlike regular RRSPs, from which you can withdraw funds (and pay tax) if you need it at any time, LIRAs generally prohibit you from making any withdrawals before 55. Granted, when you’re younger that prohibition — illustrated above as a locked piggy bank — may seem frustrating but the idea is to protect our future retired selves from our current “tempted to spend it all” current selves.

As TriDelta Financial wealth advisor Matthew Ardrey told me, you’re going to see a lot more about LIRAs in the coming years. Whether you’re leaving a classic Defined Benefit pension plan or a more market-tied Defined Contribution pension plan, the job market these days is in such flux that a lot of people are going to have to start learning about what happens when you leave an employer pension plan earlier than you might once have envisaged.

LIRAs will multiply as Boomers reach Findependence

In the case of leaving an employer that provided you with a DB pension, you’ll be getting a lump sum based on the so-called “Commuted Value” of the pension at the time you leave (whether voluntarily or due to corporate layoffs or restructuring). I suggest that those who value the certainty of future DB pension payments plan eventually to annuitize such plans, likely the end of the year you turn 71. Continue Reading…

The TFSA and an expanded CPP means Millennials will depend less on RRSPs than the Boomers did

My contribution to the Financial Post’s first RRSP special report of the season can be found by clicking on this headline: For Boomers, the RRSP decision was easy but for Millennials, things are a little more complicated. The piece, which also appeared on page FP 10 of Wednesday’s print edition, recaps the three big advantages of RRSPs, articulated by regular Hub contributor Adrian Mastracci.

As baby boomers, both my wife and I have maximized contributions to our RRSPs almost from the moment we entered the workforce in the late ’70s (actually, in my case, only since 1984, when I rolled over a Defined Benefit pension into my first RRSP). And with no employer pension plan, my wife has continued to maximize her RRSP, to the point some of my sources tell me it’s time to stop, if we don’t wish to be subjected to onerous taxations and OAS clawbacks once we reach our 70s.

As for Millennials, the FP piece makes the argument that the Millennials enjoy two things the Boomers did not have for most of their investing careers: the Tax-free Savings Account (TFSAs, the Canadian equivalent of America’s Roth plans), and second, the newly expanded Canada Pension Plan or CPP.

As I noted in a Motley Fool special report in the fall, by the time the expanded CPP fully kicks in around the year 2065, someone who qualifies for maximum benefits and waits till 70 to receive them could get as much as $2,356 a month just from CPP, or $4,712 a month for a qualifying couple. Add in a giant untaxed TFSA and that might be all they’d need in retirement: assuming this high-saving couple maximized TFSA contributions at $5,500 a year (plus any inflation adjustments to come) from age 18 on.

To be sure, the eternal (well, eternal since TFSAs were introduced in 2009) question of TFSA, RRSP or both will depend on earning levels and tax brackets, which the FP article goes into in some depth. And it also bears mentioning that the TFSA advantage would be almost twice as compelling if the Liberal government had not acted to cut back on the $10,000 TFSA limit we enjoyed one year back to the current inflation-adjusted level of $5,500. So as it stands, high earners have roughly four times as much annual RRSP contribution room as they do for TFSAs, which is a pity.

My personal inclination is to maximize BOTH the RRSP and TFSAs, which certainly should be possible if you’ve eliminated all forms of consumer debt. Most dual-income couples should be able to do both, in my view, although of course if one of them is taking temporary stints outside the workforce (perhaps for child-raising), income-splitting practices like using spousal RRSPs may make sense.

Motley Fool blog on possible ban of trailer commissions