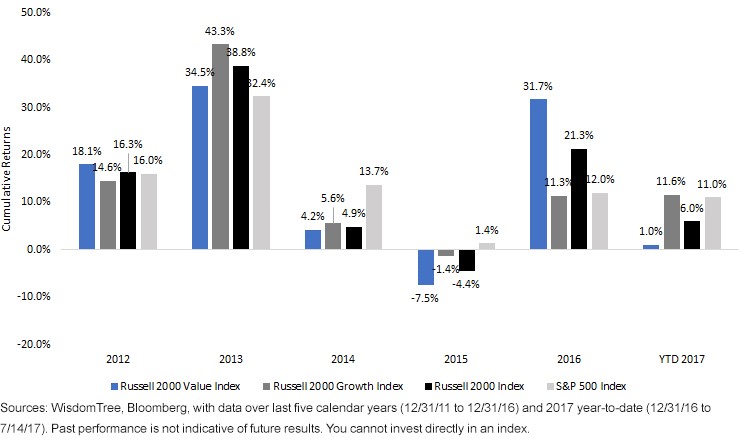

A lot of Canadians seem to be harbouring misconceptions about the value of RRSPs (Registered Retirement Savings Plans) but I can give you a million reasons why it’s dangerous to believe the five popular RRSP myths. My latest two blogs in the Financial Post this week explain why.

A lot of Canadians seem to be harbouring misconceptions about the value of RRSPs (Registered Retirement Savings Plans) but I can give you a million reasons why it’s dangerous to believe the five popular RRSP myths. My latest two blogs in the Financial Post this week explain why.

In Thursday’s Post, also published in some regional dailies, I described how young people can easily save a million dollars as long as they start early enough. Click on the highlighted text for the online link: How to build a million-dollar RRSP: it isn’t as hard to get there as you think.

Yes, it’s the old story of disciplined saving year in and year out, and the magic of compounding, all aided by the lure of an upfront tax refund and a multi-decade deferment of taxes. Of course, eventually it will be time to draw an income and pay some tax on the RRIF but that’s a story for another day.

Whether a million is enough is open to debate but with today’s paltry interest rates and rising expectations for long lives, the need for annuities or some form of longevity insurance has become urgent. More on that shortly.

Exploding 5 RRSP myths

This morning, Friday, the FP also ran a blog by me commenting on tax guru Jamie Golombek’s debunking of five common myths average investors harbour about RRSPs. You can find Golombek’s column here: The 5 biggest RRSP myths Canadians can’t stop repeating.

This morning, Friday, the FP also ran a blog by me commenting on tax guru Jamie Golombek’s debunking of five common myths average investors harbour about RRSPs. You can find Golombek’s column here: The 5 biggest RRSP myths Canadians can’t stop repeating.

My take on it and a CIBC poll that accompanied the report, can be found here: Almost 40% of Canadians see ‘no point’ in investing in RRSPs — Here’s why they’re wrong.

In short, Golombek and I agree that the RRSP makes a lot more sense than investing only in taxable (non-registered or “open”) accounts. And while the TFSA is a compelling alternative to RRSPs for young people in low tax brackets, or for low-income seniors counting on living on Old Age Security, for the vast majority of middle- and upper-middle-income private sector workers lacking a Defined Benefit plan, the RRSP remains an essential tool for building wealth.

And as I also point out, if you’re in a high tax bracket, you don’t have to choose between an RRSP and a TFSA: you should maximize both!