For the first 30 or so years of working, saving and investing, you’ll be first in the mode of getting out of the hole (paying down debt), and then building your net worth (that’s wealth accumulation.). But don’t forget, wealth accumulation isn’t the ultimate goal. Decumulation is! (a separate category here at the Hub).

My latest post at MoneySense.ca is headlined “CRA TFSA crackdown no cause for alarm.” Click through for the full piece. While you’re at it check out this post from the Hub recapping Tuesday’s one-hour live web chat with myself and Financial Post columnist Garry Marr, who has been breaking the stories about the CRA’s crackdown on excessively traded humungous TFSAs. The crackdown drew plenty of comments and suggestions.

For one-stop shopping purposes and convenience, I reproduce below the original text for my MoneySense blog on how investors should react to this crackdown.

Only minority targeted in CRA crackdown; keep maxing out your TFSA early in January

By Jonathan Chevreau

Tax Free Savings Accounts (TFSAs) have come in for a drubbing lately, based on various media reports of a CRA “crackdown” on frequent traders who have racked up excessive gains.

On social media there seem to be a lot of ordinary investors taken aback by this, even though as I have said on Twitter, 99.99% of the almost 10 million Canadians who have a TFSA hardly need to worry about this obscure attack on a few sophisticated frequent traders of speculative stocks in their accounts.

Anyone who holds index funds, ETFs, blue-chip stocks or fixed income and is holding for the proverbial long term should stick with their plans for using their TFSA, including making a full maximum contribution early in January. Frequent online traders making dozens of trades a day are the target, especially if their trading patterns causes the CRA to view them as running businesses inside their TFSAs: if you or I traded that often we’d be losing a lot in trading commissions, even at the $5 or $10 a pop that most online brokerages charge.

As I have also pointed out, TFSAs are the mirror image of the RRSP, which has been around more than half a century. Even if there is a way to define what an “excessive” gain is, does this mean Ottawa would go back through half a century’s worth of deferred RRSP gains? It seems hardly likely.

TFSA remains best game in a highly taxed town

This is really a tempest in a teapot and I’d hate to think anyone scared off by this would fail to top up their TFSA early in January. As I’ve also said more than once, the TFSA is just about the best game in an otherwise highly taxed town. And as I said in this blog a few weeks ago, the uncovering of an end run that lets the wealthy contort their finances so as to collect for three years the Guaranteed Income Supplement (intended for the elderly poor) suggests that either GIS or TFSA rules or both may get tinkered with sometime in the next few years. So it’s best to fill up TFSAs while you can, just in case Ottawa starts to curtail their use for whatever reason. And that includes maximizing your children’s TFSAs if you’re able.

To be safe, check the CRA’s 8-point audit list

The Canada Revenue Agency has rolled out an 8-point list for a TFSA “audit” but a quick scan of the items should reassure ordinary investors that there’s little cause for alarm. I can see how some knowledgeable do-it-yourself investors who love to research stocks and spend time at their trading terminals might feel a bit uncomfortable but it’s pretty clear the CRA is more worried about those who make many (10 or 15 a day) trades and who quickly liquidate their positions. Also on the list are speculative non-dividend paying stocks, people who use margin or debt to leverage their positions, and those who advertise their willingness to purchase certain securities: again, well outside the realm of the ordinary investor trying to create a little tax-free dividend or interest income. For most TFSA holders, danger is lack of capital gains not excessive ones

The irony about all this attention to a handful of professional speculators gaming the system for spectacular capital gains is that far too many TFSA users are doing the precise opposite. If all you do is go with a default GIC or low interest-bearing investment in your TFSA, then you’re not doing this vehicle justice. Chris Cottier, a Vancouver-based investment adviser with Richardson GMP, says any young investor with large debts – especially high-interest credit-card debt – should forget about TFSAs until they’ve eliminated that debt.

Very few investments can create gains greater than those accruing to those who pay off credit-card debt that approaches 20% per year.

But when are debt-free (except the mortgage), you’ll be better off holding equities in your TFSA than fixed-income investments sporting today’s minuscule interest rates.

MoneySense has long espoused a passive “Couch Potato” approach to investing in broadly diversified portfolios spread over geographies and multiple asset classes. That approach is particularly apt for TFSAs and is clearly the polar opposite of the type of investor the CRA is looking for.

So when January rolls around, do not hesitate to max out your TFSA contribution for the year 2015 and if it’s a quality ETF from a well-established manufacturer, I wouldn’t waste a minute’s thought on the CRA.

Jonathan Chevreau is Chief Findependence Officer for FinancialIndependenceHub.com.

I haven’t noticed many changes since Scotiabank bought out ING Direct in 2012, except for two:

They changed the name to Tangerine

Why did they do this? Is it a fruit? Is it a colour? WHY? People like my parents already think ING is a fake bank that will steal all my money: calling it something as light and fluffy as Tangerine does not help my case that it is a real bank with real interest rates, and that banks with tellers and real estate are as 20th century as AOL.

I will forgive them, however, because CEO Peter Aceto told Canadian Business that they weren’t allowed to use the name ING anymore. Here’s the rationale behind that decision:

“Simplicity”and “innovation”were two things the bank wanted to come across in its new name—the idea was to hearken back to its earlier days (being an alternative, simplified place to do your banking), but push the brand forward at the same time. The name Orange was considered on the shortlist, but was considered to be “too safe or obvious of a choice.”Tangerine makes reference to ING Direct’s orange history, (Ed Note [DK]:by orange history, do they mean just using the colour orange? How does a bank have colour history?) while also being significantly different.

Aceto says part of the branding discussion also took into account the more “fun”aspects of the name.

“We understood the risk that a name like that could be interpreted as being silly, or not serious,”he says. “Banking is important, it’s serious. We’re asking you to give us your life savings, or to help you buy a home or invest.”

That’s why there won’t be any references to fruit in any of Tangerine’s advertising materials or promotional campaigns. The fun name “does a lot of work for us”in sparking interest in Tangerine, Aceto says, but service at the customer level needs to be thoughtful and earnest in order to build a client base.

“I want people to think, oh, they’re different. They’re not like everyone else.”

They changed the debit card by making it flimsier and WRONG

Writing the bank name horizontally across a debit card made sense when we signed for things.

Now we use a chip and PIN# method of payment. The chip is always entered vertically.

So why, on all debit cards, is the bank name still horizontal?

ING was the only card to write its name vertically, which was logical and made them seem the most current.

With the buyout, it has gone backwards and written its company name horizontally.

Also, while you can’t see this in a picture, the new card is very flimsy and bendy. It’s not really a problem but coupled with Tangerine it just kind of makes the bank seem flimsy.

Now, these are all personal pet peeves that have no affect on how they do business; banking with them hasn’t changed. They don’t have the best interest rates anymore; that award would go to credit unions in Western Canada, but they are still way better than the Big Five banks and they also have lower fees (no fees!) than the credit unions.

All in all, it’s still my favourite Canadian bank with which to do my daily banking, but it’s no longer my favourite choice with which to invest in GICs, which will be the subject of another post.

Here’s how this article originally appeared at Danielle’s Pretty Little Poor Girl blog. And you should click on the link because apart from Danielle’s awesome slogan, she includes an extra paragraph at the bottom of her original post that further teases the good folks at Tangerine: JC.

If you missed the one-hour live web chat about Tax Free Savings Accounts (TFSAs) at the Financial Post, you should be able to read the transcript here. It was a fairly spirited chat, seeing as Garry and the Post have been breaking story after story lately about the CRA’s move to audit overly aggressive, excessively traded TFSA accounts with massive gains in them.

At the other end of the scale, and as Garry has pointed out, the big losers in TFSAs tend to be those who take the GIC default products and end up making it paltry 1 or 2% in interest income. Even worse, as GMP Richardson’s Chris Cottier has pointed out, are those making this pittance in the TFSA while paying out upwards of 20% in credit-card charges.

Also on the chat presenting the financial industry’s perspective was Rubina Ahmed-Haq. The chat was sponsored by PC Financial.

Many consider defined benefit pension plans the gold standard of retirement plans. Through the ups and downs of the markets, defined benefit (DB) pension plans remain the one thing that employees can count on in their golden years. DB plans offer employees some much-needed stability in retirement. For those without the luxury of an employer-provided pension plan, the alternative is RRSPs. With RRSPs, you contribute throughout your career and hope that your investments perform well enough so you can enjoy a comfortable lifestyle in retirement.

Defined Benefit Plans Disappearing

While workplace DB plans used to be widespread in the private sector, they’ve been disappearing at an alarming rate over the last couple of decades. Now only a third of employees have any kind of pension plan at work, let alone a DB pension plan. The dot com bubble in 2001 and the financial crisis in 2007 only sped up the pace at which employers are looking to “de-risk.” De-risking comes in many forms, but the most prevalent is switching from a DB plan to a defined contribution (DC) plan or group RRSP.

Defined Benefits vs. Defined Contribution

With a DB plan the employer bears most of the investment risk. If investments underperform, it’s up to the employer to make up any shortfall. However, with a DC plan or group RRSP, employees bear the brunt of the risk. If their investments don’t pan out, they’ll have to make tough decisions like scaling back their lifestyle in retirement or working longer (if they’re physically able to).

Having worked as a pension analyst at a global pension and benefits consulting firm for nearly five years, I have a unique perspective on what’s been unfolding in the realm of pensions. I’ve watched as pension plans on which I work have closed DB pension plans to new entrants, forcing new hires to enroll in DC plans. Although I still have a DB plan at work, even my own plan has been scaled back in recent years.

How do DB Plans Fit into My Findependence?

That brings me to the main point of this article: are DB plans part of my own Findependent plans, or I am so much into self-employment and Internet businesses that I feel they’re okay for really conservative members of my generation, but perhaps not for myself? Despite working as a financial journalist to supplement my income, I still see DB plans as an integral part of my Findependent plans.

Even though I don’t plan to retire until at least age 55, it’s still nice to know I have a guaranteed DB plan waiting for me when I do decide to call it a career. A DB plan will provide a large chunk of my money in retirement. Because of that, I’ve been able to invest more heavily in equities in my RRSPs.

I’m a big fan of the Canadian Couch Potato investment philosophy. I chose the TD e-Series funds because of their great track record and low fees. I’m invested heavily in equities – I have 30% invested evenly in Canadian, U.S. and International equities, with only 10% in bonds. I wouldn’t have been able to take this position without a rock-solid DB plan waiting for me.

What About Everyone Else?

If you’re a younger worker in an industry where you plan to change jobs every few years, a DB plan probably doesn’t make much sense. But if you’re someone like me who’s willing to spend their entire career at a company once they find a job they love, a DB plan can be a great way to build up your retirement income as a reward for your years of service.

Some people refer to DB pension plans as pyramid schemes without getting the facts straight. For the most part your company pension plan is safe. Workers in Ontario have added protection – up to $1,000 of your monthly protection is guaranteed by the government.

Would I ever consider trading in my DB plan? Not a chance. I see my DB plan as an important part of my journey towards Findependence. I know I can count on it when it matters most.

Sean Cooper is a Personal Finance Expert and Financial Journalist. He is a first-time homebuyer and landlord who aspires to reach findependence by age 31. Follow him on Twitter @SeanCooperWrite and read his blogs and request his writing services on his website: http://www.seancooperwriter.com/

Making smarter investment choices is one of the key elements in building up adequate retirement savings. [1] People are constantly inundated with sales pitches for investment opportunities from banks, insurance companies, and their friends and relatives. For those with limited investment knowledge, this can be intimidating. The natural inclination is to seek advice from a professional investment advisor; however, many investment advisors may be motivated to recommend the investment vehicles that pay them the highest commission. In this environment, it’s wise for individual investors to have a basic knowledge of investments. This paper aims to provide seven fundamental principles that should lead to smarter investment decisions.

1. Ignore ‘hot’ investment tips

Investments are inherently risky; some have lower risk, others have higher risk. It is socially common for co-workers, friends, or relatives to announce that they have the inside scoop on an investment opportunity that is going to have a high return, if it is acted on immediately. To compound this, people tend to discuss their winning stock picks publicly, but do not readily disclose their losers. The media often provides flashy investment advice that may not be right for a vast majority of investors, while sensationalizing world events in the context of stock markets. There are constant psychological triggers to buy and sell securities without adequate knowledge built into everyday life, and acting on these triggers can be the single biggest threat to the long-term financial health of an investor.

Conclusion: Acting immediately on information from friends, family, and the media may lead to a bad investment experience.

2. Have a basic knowledge of investment vehicles

There are many ways for individuals to invest their savings in financial markets. The most common ways to invest include stocks and bonds, mutual funds, and exchange traded funds (ETFs).

Individual stocks and bonds are inherently risky investments requiring in-depth knowledge of the underlying company being considered. It is highly unlikely that individual investors will have the time, background, or resources to conduct the necessary analysis on enough companies to build a portfolio that is positioned to outperform a passive investment in a benchmark index – even professional money managers have trouble achieving this consistently[2]. An alternative is to invest in a basket of stocks and bonds in such a way that diversifies away the risk associated with any individual company. The exact number of securities that it takes to build an optimally well-diversified portfolio is up for debate, but it is safe to say that buying a handful of stocks and hoping for the best is not ideal.

Mutual funds are vehicles that allow investors to obtain a well-diversified portfolio through a pre-packaged product. For this service, investors pay a fee to the mutual fund company, referred to as management expense ratio (MER). The MER pays for the fund’s manager and other expenses. Many mutual fund companies claim that their managers have special predictive insights and the ability to find stocks that are poised to increase in price more than their peers. These actively managed funds have significantly higher fees than a mutual fund that simply buys all of the stocks in an index, called an index mutual fund, or index fund. The high fees paid to actively managed mutual funds could be warranted if they produced superior performance, but an overwhelming amount of evidence shows that superior long-term performance is not likely[3]. Currently, 98.5% of the assets invested in Canadian domiciled mutual funds are invested in actively managed mutual funds[4].

ETFs, like index mutual funds, invest passively in an index. ETFs tend to have much lower fees than mutual funds due to their underlying structure, while still allowing investors to invest in a well-diversified basket of securities.

Conclusion: It is not practical for the average investor to build a well-diversified portfolio using individual stocks and bonds. There is sufficient empirical evidence to show that actively managed mutual funds, on average, do not show any superior performance over index mutual funds. Investors are likely better off investing in index ETFs or low cost index mutual funds.

3. Understand the risk-return trade-off

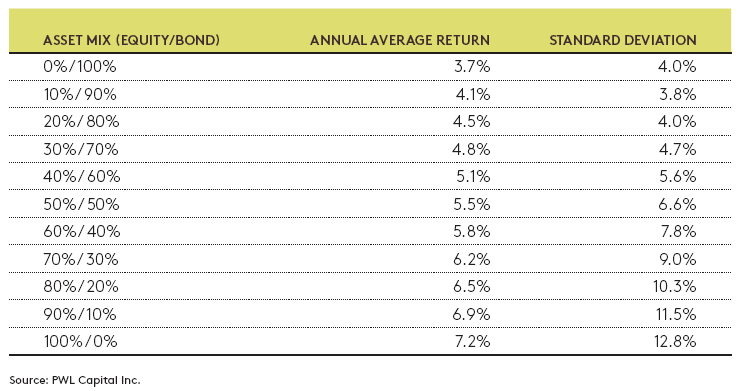

Most investors build their portfolio using some mix of stocks and bonds; this is known as their asset mix. Stocks tend to be riskier than bonds, as measured by the standard deviation of their returns. Riskier investments must have higher expected returns to attract investors, and it follows that stocks must have higher expected returns than bonds.

In a recent white paper, PWL’s Raymond Kerzerho and Dan Bortolotti used historical data and current market expectations to demonstrate the expected returns for portfolios with various mixes of stocks and bonds. The results demonstrate the relationship between risk and return – portfolios with higher expected returns also have a higher expected standard deviation. Statistically, it can be expected that in 65% of trials, the returns of a portfolio will fall within one standard deviation of the average return; in 95% of trials, the portfolio returns will fall within two standard deviations of the average return.

To ensure a desirable risk-return expectation, investors must decide how much volatility they are willing to bear, while understanding that less volatility means lower long-term expected returns. Selecting the right asset mix is one of the keys to sticking with an investment plan.

Conclusion: Higher returns are associated with higher risk, as measured by standard deviation. Investors need to understand, and be comfortable with, the risk and return expectations of their portfolio.

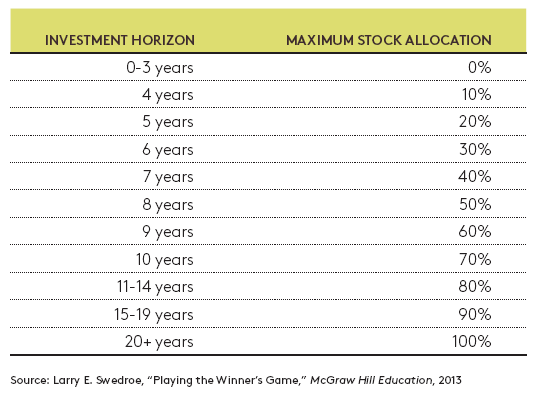

4. Know your time horizon

In a given year, the return on a portfolio has a 95% chance of being within two standard deviations of the expected average return. As an example, the one year return on a 60% equity, 40% fixed income portfolio could be expected to fall between -9.8% and 21.4%. If an investor has a one year time horizon, this wide range of returns is not likely to be suitable. As the investor’s time horizon gets longer, it becomes more likely that the realized average return on the portfolio will be close to the expected average return. Investors can have different time horizons for various investment goals, but the funds associated with each goal must be invested appropriately to achieve a successful investment experience. In his book, Playing the Winner’s Game, Larry Swedroe outlines some suggested asset mixes based on investment time horizon.

Conclusion: A long time horizon gives investors the ability to withstand the short-term volatility that accompanies the higher expected returns of stocks. A short time horizon means that less risky investments must be chosen to avoid realizing losses.

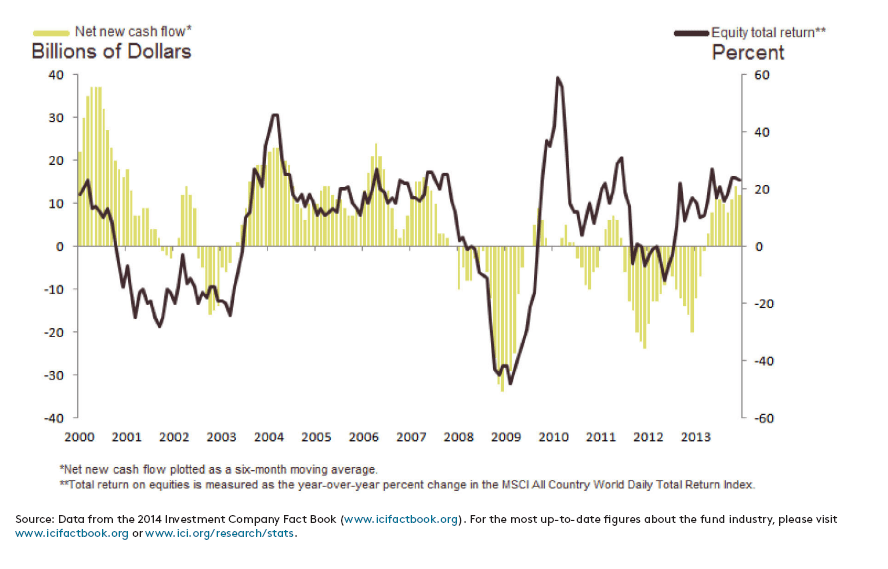

5. Focus on time in the market, not timing the market

Timing the market is the action of timing buy and sell decisions in an attempt to gain additional profits by buying low and selling high. Data for US mutual fund cash flows and global equity returns from the Investment Company Institute shows how investors tend to fare at market timing; when markets were doing well, investors were pouring money into equity mutual funds, and when markets were doing poorly they were selling. This buying high and selling low behaviour is driven by the fear and greed that underlie investor psychology. These actions have extremely negative effects on the performance of a portfolio.

A simple solution to avoid market timing impulses is dollar-cost averaging, systematically investing the same amount each month. This method of entering the market alleviates the stress associated with market timing, and suits investors with a fixed amount available to invest each month.

Some investors may have a large lump sum to invest from a settlement, prize, or inheritance. Research from the Vanguard Group has shown that approximately two-thirds of the time, lump sum investing has resulted in superior risk-adjusted performance as compared to dollar-cost averaging[5]. Based on this research, if an investor is comfortable with their asset mix and its risk and return characteristics, it is statistically prudent to invest the full lump sum immediately. If the investor is more concerned about protecting against short-term losses and feelings of regret, then dollar-cost averaging is appropriate.

Conclusion: The simplest solution for investors to avoid market timing is to invest the same amount every week, month, or quarter without worrying about the short term movement of the market. When lump sum investing is deemed appropriate, the investor must be comfortable with the risk/return characteristics of their portfolio.

6. Costs impact wealth accumulation

If an investor decides to invest in an actively managed mutual fund, they are subject to management fees, which are especially high in Canada[6]. The fees, typically in the range of 1.5 to 2.5% of the account value on an annual basis, have a significant impact on wealth accumulation[7]. This can be best illustrated with an example. Assume that both an active mutual fund (2% annual fee) and a passive ETF (0.5% annual fee) generate the same long-term investment return, less their fees. If the market produces an assumed rate of return of 5% over 25 years, and an investor invests $10,000 each year in an RRSP, the value of the savings invested in the active mutual fund would be $364,593, whereas the value of the passive ETF investment would be $445,652. This is a difference of $81,059, or 18%, in favor of the low cost passive investment.

Conclusion: Costs can have a dramatic effect on wealth accumulation. Ask for all possible fees to be disclosed when working with a professional, and look for investments with low upfront and ongoing costs.

7. Utilize tax advantaged accounts

In Canada, we have a handful of tax advantaged accounts that can be used to hold qualified investments. The various accounts have different purposes, but both large and small investors can benefit from using them. For a long-term investor planning for retirement, two of the most useful account types are the Registered Retirement Savings Plan (RRSP), and the Tax Free Savings Account (TFSA).

Contributions to the RRSP are deducted from taxable income in the year they are made, in most cases result ing in a tax refund. Investment growth and income build inside the RRSP tax free, and any withdrawals are taxed as income in the year they are withdrawn. The idea is that investors will contribute when they are in a high tax bracket, and withdraw when they are in a lower tax bracket. RRSP room builds based on 18% of the previous year’s earned income and can be carried forward indefinitely.

For the TFSA, there is no deduction from taxable income when money is added to it, and there is no tax payable on withdrawals. Like the RRSP, investment income and growth build tax free. Every Canadian resident starts building TFSA room when they turn 18, and currently all eligible people build $5,500 of new room each year.

Until both these accounts have been maximized, there are very few logical reasons to start investing in taxable accounts.

Conclusion: Before investing in taxable accounts, maximize the user of registered, tax-advantaged savings plans.

Becoming a smart investor

Acting on these principles is likely to be beneficial, but they all need to be tied together with a clear investment strategy. One method for sticking to an investment strategy is the creation of an Investment Policy Statement (IPS), which becomes a guideline for future investment decisions.

The IPS is created based on risk-return requirements, time horizon, and investment preferences; it sets rules for how much of each type of security should be held. An example of an IPS could be 20% Canadian stocks, 20% US stocks, 20% International stocks, and 40% bonds. When designed thoughtfully, an IPS allows the investor to separate their emotions from buy and sell decisions, instead basing decisions on the predetermined rules. When the portfolio strays from its targets due to market movement, it must be rebalanced to match the allocations set out in the IPS.

With a strategy in place, a smart investor will revisit their personal situation periodically (annually at least) to see if they should be modifying their IPS or their holdings. It is possible that new investment vehicles with lower costs or increased tax efficiency have been introduced, or that the investor’s time horizon or risk tolerance has changed due to a life event. Managing the optimal use of tax advantaged accounts must also be revisited periodically.

Tying these seven principles together and sticking to a consistent and methodical strategy can result in a pleasant, stress free investment experience, and long term wealth creation.

[1] Vijay Jog, “Investment Performance and Costs of Pension and other retirement Savings Funds in Canada: Implications on Wealth Accumulation and Retirement,” Department of Finance Canada, 2009

[2] Mark Carhart, “On Persistence in Mutual-fund Performance,” Journal of Finance, March 1997

[3]Aye M. Soe, “The Persistence Scorecard,” S&P Dow Jones Indices, June 2014

Tax Free Savings Accounts (TFSAs) have come in for a drubbing lately, based on various media reports of a CRA “crackdown” on frequent traders who have racked up excessive gains.

Tax Free Savings Accounts (TFSAs) have come in for a drubbing lately, based on various media reports of a CRA “crackdown” on frequent traders who have racked up excessive gains.