By Alyssa Furtado, RateHub.ca

Special to the Financial Independence Hub

Interest rates in Canada have rarely seen such lows, which makes borrowing money to buy a home pretty attractive. But when you start looking around for the best mortgage rates, homebuyers face a choice of going with a variable-rate or a fixed-rate mortgage.

So what’s the difference? A variable-rate mortgage follows interest rates as they move up and down. And a fixed-rate mortgage is locked in for a certain term. Sounds simple, but deciding which option works for you can depend on a number of factors. Here are some essential pros and cons:

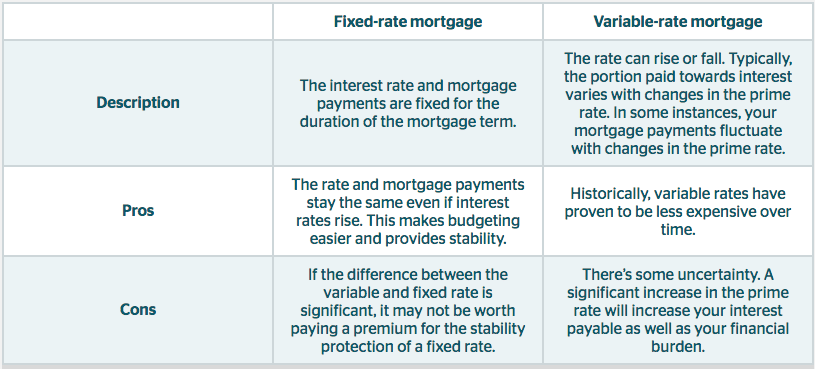

Fixed-rate mortgages

Pro: Added security

You don’t have to worry about whether your payments will change because of economic factors you can’t control during the mortgage term. This makes long-term financial planning much easier.

Say you get a five-year fixed-rate mortgage, with a 2.5% interest rate. Regardless of whether interest rates go up or down elsewhere, the rate will stay at 2.5% for the entire five-year period. This allows you to set it and forget it until it comes time to renew your mortgage, at which point you’ll need to renegotiate your rate. At this point your rate could be higher or lower.

Con: Added expense

The luxury of knowing your rate will remain the same will likely cost you, as fixed rates tend to be higher overall.

Variable-rate mortgages

Pro: You can save a bundle

Although by no means guaranteed, historically borrowers save more money over time with this method. Your rate is correlated to the prime lending rate, which can fluctuate. Your rate is quoted as the prime rate plus or minus a certain percentage, such as prime minus 0.4%. In this instance, if the prime rate is 2.7%, your mortgage rate will be 2.3%. Such a small percentage might not look like it will affect your payments, but the savings will add up significantly over time.

Con: Rates can always go up

The variable-rate option comes with a certain risk. If your bank’s prime lending rate changes, the interest moves up or down in conjunction with it. The amount you actually pay your lender on a regular basis (biweekly, monthly, etc.) won’t necessarily change. If the interest rate goes down, more money from your payment will go toward paying down the principal. If the rate goes up, more of the payment will be eaten up by interest, and sometimes your regular payment can also rise. Continue Reading…