“Motivation is what gets you started. Habit is what keeps you going.” —Jim Ryun, Olympic runner

We’re working our way through the fourth quarter 2017. Many stock indices have been hovering near their tops and often keep making new highs. Daily headlines are typically a mixed bag of fears and optimism. They are often interpreted as indications of possible changes in market direction.

Some themes really stand out. For example, NAFTA talks are topics du jour in the US, Mexico and Canada. The United Kingdom is wrestling with Brexit implications. German politics are entertaining altering the seating arrangements.

Many stock indices hover near their tops and keep making new highs.

China faces pressures from increasing debt levels. US tax cut battles keep marching along. Several faces will soon change at the US Federal Reserve. Rising interest rate discussions send chills down the spines of borrowers. These few points alone are forceful enough to create trepidation in investor minds. You will have no difficulty finding headlines for every investment neighbourhood.

As a result, investors develop itchy fingers that want to migrate to the safety of the sidelines, whether it’s beneficial or not. Of course, these investors that have the need for action will make the crucial timing calls on what to buy or sell. Everyone should know by now that timing the markets is a low percentage approach, fraught with many dangers.

My Observation

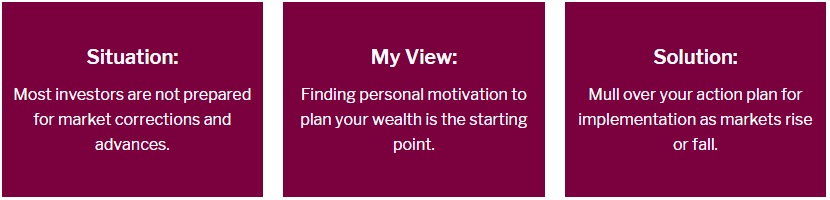

This brings me to one important observation. Wise investors are in the habit of investigating what it takes to be well prepared for both market corrections and advances. They have at least sketched out a rough game plan for each case on the back of the napkin. Something to get started, aiming for the right path. I encourage you to become conversant with what you would likely do with stocks and bonds during bullish and bearish markets.

Most investors that think in this fashion prefer to have some framework of how to approach the uncertainties that come their way. Just some simple ideas are required to get started. The best news is that today’s planning is being conducted while stock prices are high.

Finding the motivation to be informed is a welcome initial step. Perhaps, discussions with your investment professional will shine more light on what actions are in your best interests. Reconfirming your family risk profile is also time well spent. Hopefully, these efforts lead to more disciplined planning for the precious nest egg. The main mission is to reach and deliver your retirement objectives.

Seasoned investors are well aware that diversification and rebalancing strategies are part and parcel of this logical planning approach. I cannot emphasize that enough as nobody knows where the markets are headed or when a directional turn comes around the curve. Bells do not ring when the time is ripe to make portfolio changes. Neither at the top, nor at the bottom.

My Recommendation

I suggest mulling over these situations in preparation for your exercise: Continue Reading…