By David J Rotfleisch, CA, CPA, JD

By David J Rotfleisch, CA, CPA, JD

Special to the Financial Independence Hub

The proposed changes to the Income Tax Act that the Minister of Finance, the Honourable Bill Morneau, has released have real-world implications. The consultation period ends October 2, 2017, so now is the time to make your voice heard. Call or email your member of Parliament, or Minister Morneau directly.

I recently had a meeting with a high-tech entrepreneur in an internet-based business. He is very conservative and has not carried out any tax planning. His wife helps him but he does not do any income splitting with her. He has about $1 million in his corporate bank account for possible business use, but has not invested it and just earns minimal bank interest. The hype about the proposals has caused him to take notice of his tax affairs and meet with me.

I told him that under the new proposals income splitting with his wife, other than a fair salary for services performed, will be prohibited. His wife will probably not be able to participate in the lifetime capital gains exemption. If he decides to invest his retained earnings, there may be an additional tax on his income. He is now thinking about lifestyle and whether he wants to leave the country. I fully expect to prepare a memo for him about becoming non-resident.

Minister Morneau’s proposed tax changes will have the effect of causing an exodus of Canadian entrepreneurs for more business-friendly jurisdictions.

I had lunch with accountants a few days ago and they reported the same types of conversations with high-tech clients. They are considering leaving the country. Now, some won’t because of the education of their children, to be close to aging parents, adult children,or because they like their Canadian lifestyle. Others will decide it’s more important to maximize after-tax income and that it makes sense to move offshore.

70% of Canadians work for firms with 100 or fewer employees

Remember, statistics show that the vast majority of Canadians — 70 per cent — who are the economic engine of this country, work for companies with between 1 and 100 employees: the very targets of these new measures, and who are able in many cases to pack up and leave.

This is not just the view of tax professionals. Ryan Holmes, the CEO of social media internet company Hootsuite, was reported as saying on Sept 14, 2017 that the proposals are causing a lot of concern to business owners and that “I think you need to be very favourable at the small end of the market.”

I was recently contacted by a Liberal MP who is very opposed to what his government is doing. He has an entrepreneurial background and he realizes the impact of these proposals.

Continue Reading…

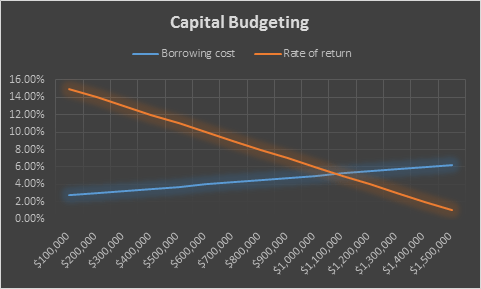

So in the example chart shown to the right, you would borrow and invest up to $1.0 million, which is the point where the expected rate of return declines to meet increasing cost of borrowing at about 5%.

So in the example chart shown to the right, you would borrow and invest up to $1.0 million, which is the point where the expected rate of return declines to meet increasing cost of borrowing at about 5%.