You’re about to make one of the biggest decisions of your life by purchasing a home. And it will likely be your biggest and most complicated financial commitment. So you should make a plan that captures everything you need to do to avoid costly mistakes.

Here’s a list of five mistakes you shouldn’t make when purchasing your first home.

1.) Failing to get pre-approved for a mortgage

It’s vital you know how much you can spend before you start looking for your first home. To figure out how large of a mortgage you can afford, use a mortgage affordability calculator. This will help estimate how much you will be pre-qualified for by a lender, who will conduct a credit check and review your finances. You can arrange for your pre-approved mortgage rate to be held for a period of about 90 to 120 days while you search for the right property.

2.) Not researching mortgage rates

Your first instinct will be to approach your current bank to obtain a mortgage, but you should do some research first to find the best mortgage rates. Continue Reading…

Does the notion of grinding it out day in and day out for the next 40 years to experience the freedom of retirement scare you? Wouldn’t you rather strive to enjoy the journey along the way?

The good news is that the traditional concept of retirement is slowly dying.

With the elimination of most employer pension plans and the fact that humans are living longer than ever, we are forced to come up with a different take on how our parents/grandparents view retirement.

Today I’ll show you two different concepts that rethink our traditional retirement model and are gaining popularity amongst the next generation of workers.

Findependence

What’s Findependence? It’s a term coined by Jon Chevreau: author, former editor-in-chief of MoneySense Magazine and founder of the Findependence Hub, an online platform and community for curated content focusing on achieving Financial Independence. “Findependence” is simply a contraction of the phrase “Financial Independence.”

Financial Independence is the point at which you work because you want to, not because you have to. It’s the tipping point where you have the right level of savings and investments working for you to provide the income you need to live your ideal life.

Think about that. It sounds very similar to our definition of retirement and at the same time totally reframes the perception of what retirement should entail. Rather than focusing on when you can stop work forever, you now shift your mindset to creating enough passive income through investing so that you can pursue anything you want.

New research from a colleague has me thinking about hindsight. The trouble, as the saying goes, is that hindsight is 20/20 — and you can’t benefit from it after the fact.

But why not try to benefit from someone else’s hindsight? My colleague Anna Madamba of the Vanguard Center for Investor Research found in a new study that recent retirees were largely satisfied with their financial situations in retirement, but, if they could, would still do some things differently in preparation.

With the benefit of retrospect, 43% of Canadian survey respondents “agreed” or “strongly agreed” that they would have saved more — a higher percentage than garnered by any other answer.

But perhaps it’s too simple to suggest that pre-retirees should just follow the example of others. Many people know at some level that they need to save more. Whether they do often comes down to two things: competing priorities and insight into how much money they’ll have (and need) in retirement.

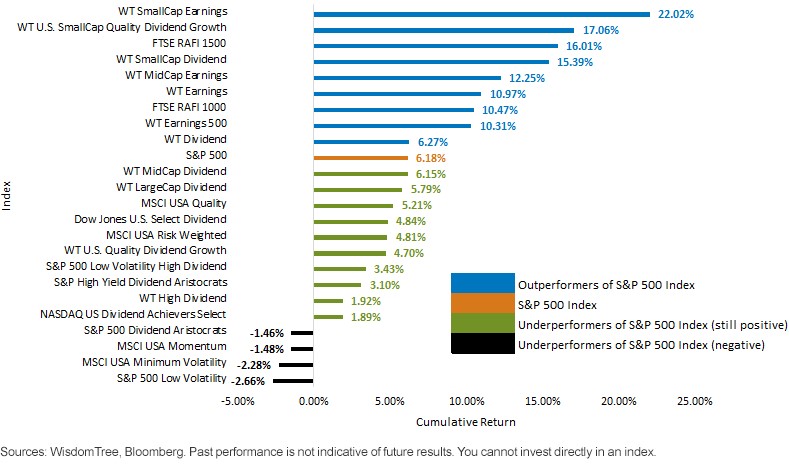

One of the biggest stories in 2016 was rising interest rates, most specifically that the U.S. 10-Year Treasury Note went from 1.36% on July 8 to 2.44% on December 31.1 While it may be too early to know if the greater than 30-year bull market in bonds (in other words, a longer than three-decade secular trend of falling rates) is over, 2016 did offer an interesting case study of smart beta strategies, many of which had only been in live calculation during falling rate periods. How Strategies won as Rates rose

In the recent rising rate periods in 2013 (May 2, 2013, to December 31, 2013, when the U.S. 10-Year yield went from 1.62% to 3.03%)2 and 2016, a few big themes became clear:

Small Caps: One aspect of small-cap companies is their ability to respond quickly to trends of improving growth, which is typically apparent during periods when the 10-Year yield is increasing. Additionally, they tend to have cyclical exposures regarding sectors instead of more defensive exposures. Also, if the U.S. dollar is strengthening (not unusual when the 10-Year yield is rising), these firms do not tend to have exports as their dominant source of revenue and therefore have less of a competitive headwind.

Earnings: Rising rates tend to place strategies with higher valuations at risk, because one impact of rising rates is to lower the current valuation multiple of equities. WisdomTree’s earnings strategies are designed to provide lower price-to-earnings (P/E) ratio exposures to the market segments upon which they focus. It’s also notable that they tend to naturally be under-weight in the more defensive sectors of the market (Utilities and Telecommunication Services are two big examples) that usually tended to do better during the falling rate periods that directly preceded the rising rate period.

How Strategies Lost as Rates Rose

• Low Volatility/Minimum Volatility: It’s important to realize that the word “volatility” relates to both upside and downside market movements, seeking to lower both of them. Continue Reading…

I recently had a chance to discuss a new Canadian advisory on dividend stocks with the people responsible for that newsletter. The advisory comes from TSI Network, founded by Pat McKeough, whose investment approach I have always respected.

The advisory is TSI Dividend Advisor (shown above), and it grew out of a long respect for the power of dividends.

Pat and his investment team have always viewed dividends as a sign of investment quality. By extension, dividend stocks become the most reliable foundation of an investment portfolio built for growing wealth and financial independence.

This confidence in dividends is accompanied by a detailed examination of dividend-paying stocks to identify those with the greatest potential to sustain, and raise, their payouts.

The 8 key points they use to evaluate dividend stocks grew into their Dividend Sustainability Ratings. This proprietary ratings system became the backbone of the new TSI Dividend Advisor. It was launched late in 2016 to impressive reviews in the media and a flood of subscriptions from Canadian investors.

Here are some of the keys to that success, from the editors’ point of view.

Jon Chevreau: First of all, Pat, thanks for your time. What role do dividends play in a successful portfolio? How can they lead to Findependence?

Pat McKeough

Pat McKeough: Top dividend stocks are a key part of a successful portfolio. Top dividend stocks can produce as much as a third of your total return over long periods. These payouts are drawn from earnings cash flow and paid to the shareholders of the company. Typically, these dividends are paid quarterly, although they may be paid annually or monthly as well.

At TSI Network, we think investing in dividend stocks is one of the best investment decisions you can make to achieve Findependence. Dividends serve as a way for companies to share the wealth they accumulate through successfully operating their businesses.

JC: Manystocks have dividends. What makes a top dividend stock?

Jon Chevreau

PM: Top dividend stocks provide steady dividends: a sign of investment quality. Some good companies reinvest profits instead of paying dividends. But fraudulent and failing companies hardly ever pay dividends. So if you only buy stocks that pay dividends, you’ll automatically stay out of almost all the market’s worst stocks. For a true measure of stability, focus on companies that have maintained or raised their dividends during economic and stock market downturns. These firms leave themselves enough room to handle periods of earnings volatility. By continually rewarding investors, and retaining enough cash to finance their businesses, top dividend stocks provide an attractive mix of safety, income and growth. Continue Reading…

By Alyssa Furtado, RateHub.ca

By Alyssa Furtado, RateHub.ca